All Categories

Featured

Table of Contents

- – What are the top Variable Annuities providers ...

- – What is the difference between an Retirement I...

- – Is there a budget-friendly Guaranteed Income ...

- – Can I get an Guaranteed Return Annuities online?

- – How much does an Retirement Income From Annu...

- – What is included in an Annuity Investment co...

Note, nonetheless, that this does not claim anything regarding readjusting for rising cost of living. On the plus side, even if you think your alternative would be to buy the stock exchange for those 7 years, and that you would certainly get a 10 percent yearly return (which is far from certain, specifically in the coming years), this $8208 a year would certainly be more than 4 percent of the resulting small supply value.

Instance of a single-premium deferred annuity (with a 25-year deferral), with four payment options. The regular monthly payout below is greatest for the "joint-life-only" alternative, at $1258 (164 percent greater than with the immediate annuity).

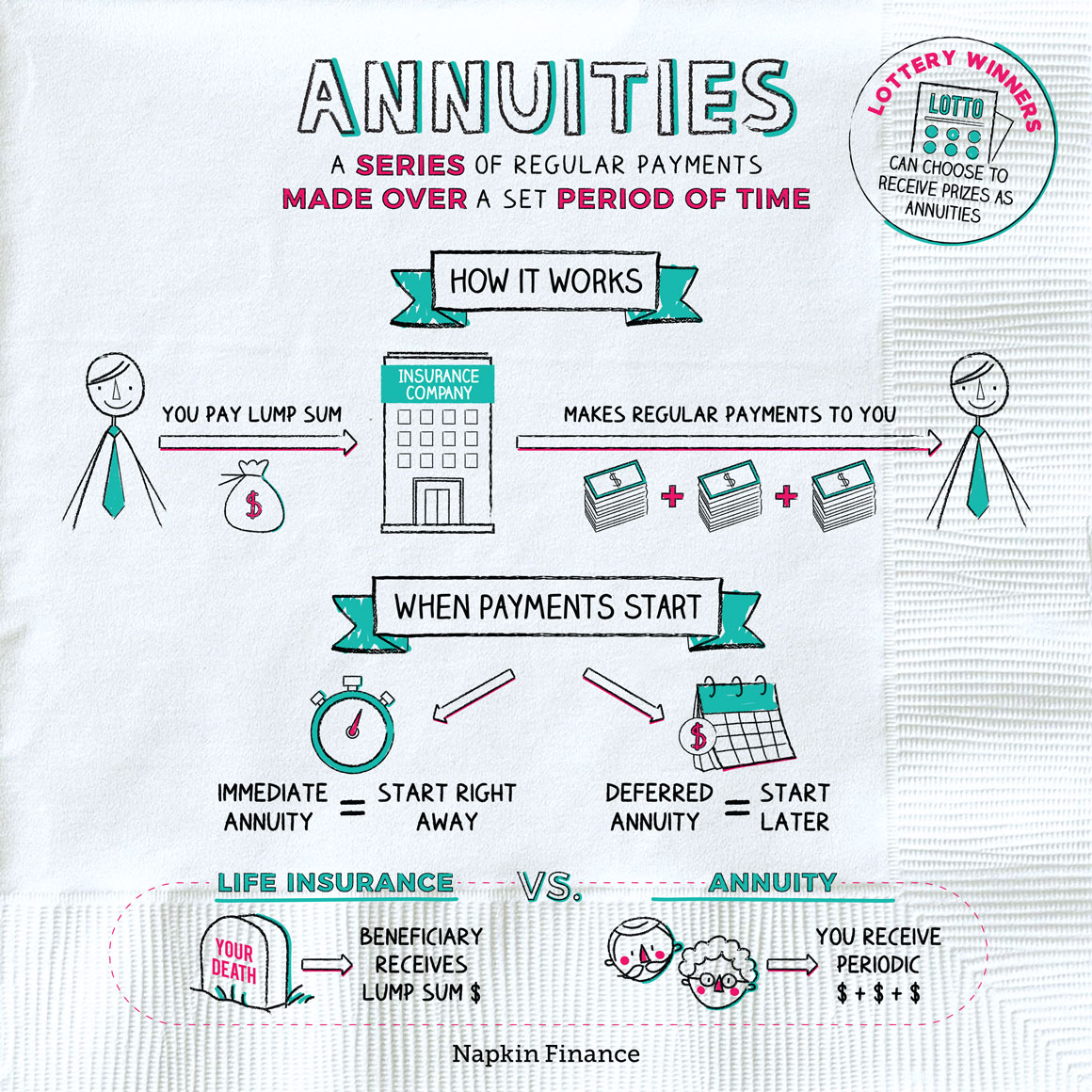

The means you get the annuity will identify the response to that question. If you purchase an annuity with pre-tax dollars, your premium lowers your taxable earnings for that year. However, ultimate repayments (regular monthly and/or swelling sum) are exhausted as routine revenue in the year they're paid. The benefit right here is that the annuity might allow you postpone tax obligations past the IRS payment limitations on Individual retirement accounts and 401(k) strategies.

According to , buying an annuity inside a Roth plan leads to tax-free settlements. Purchasing an annuity with after-tax dollars beyond a Roth leads to paying no tax on the portion of each repayment connected to the initial premium(s), yet the continuing to be part is taxable. If you're setting up an annuity that starts paying before you're 59 years of ages, you might have to pay 10 percent early withdrawal fines to the internal revenue service.

What are the top Variable Annuities providers in my area?

The consultant's initial step was to establish an extensive economic prepare for you, and after that clarify (a) how the proposed annuity suits your general strategy, (b) what options s/he taken into consideration, and (c) exactly how such choices would or would certainly not have actually led to lower or higher compensation for the consultant, and (d) why the annuity is the premium option for you. - Senior annuities

Certainly, an advisor might attempt pressing annuities even if they're not the very best fit for your situation and objectives. The reason could be as benign as it is the only item they sell, so they drop prey to the proverbial, "If all you have in your tool kit is a hammer, rather quickly every little thing begins resembling a nail." While the expert in this circumstance might not be unethical, it raises the danger that an annuity is an inadequate selection for you.

What is the difference between an Retirement Income From Annuities and other retirement accounts?

Given that annuities often pay the representative offering them a lot greater commissions than what s/he would obtain for investing your cash in common funds - Fixed-term annuities, not to mention the absolutely no commissions s/he would certainly obtain if you invest in no-load common funds, there is a large incentive for representatives to press annuities, and the more complex the far better ()

An unethical advisor suggests rolling that quantity right into new "much better" funds that simply occur to carry a 4 percent sales load. Consent to this, and the consultant pockets $20,000 of your $500,000, and the funds aren't likely to do far better (unless you picked a lot more badly to begin with). In the very same instance, the advisor can steer you to purchase a complex annuity with that said $500,000, one that pays him or her an 8 percent commission.

The expert tries to hurry your decision, declaring the deal will soon vanish. It might indeed, yet there will likely be equivalent offers later on. The expert hasn't figured out just how annuity payments will be exhausted. The consultant hasn't disclosed his/her compensation and/or the charges you'll be billed and/or hasn't shown you the effect of those on your eventual settlements, and/or the compensation and/or fees are unacceptably high.

Your family background and present wellness indicate a lower-than-average life expectations (Annuity withdrawal options). Existing rates of interest, and therefore forecasted repayments, are historically reduced. Even if an annuity is right for you, do your due diligence in contrasting annuities marketed by brokers vs. no-load ones marketed by the providing business. The latter may need you to do even more of your own research study, or use a fee-based financial expert who may receive payment for sending you to the annuity company, however might not be paid a higher compensation than for various other investment options.

Is there a budget-friendly Guaranteed Income Annuities option?

The stream of month-to-month repayments from Social Protection resembles those of a postponed annuity. A 2017 relative evaluation made an in-depth comparison. The following are a few of the most salient points. Given that annuities are voluntary, individuals getting them usually self-select as having a longer-than-average life expectancy.

Social Safety benefits are completely indexed to the CPI, while annuities either have no rising cost of living security or at many supply a set portion annual boost that may or may not compensate for rising cost of living completely. This kind of motorcyclist, similar to anything else that raises the insurance provider's danger, requires you to pay even more for the annuity, or approve reduced settlements.

Can I get an Guaranteed Return Annuities online?

Please note: This short article is meant for informational objectives only, and ought to not be thought about monetary recommendations. You should seek advice from a monetary professional prior to making any kind of significant economic choices.

Since annuities are meant for retired life, taxes and penalties may use. Principal Protection of Fixed Annuities.

Immediate annuities. Utilized by those who want trusted revenue quickly (or within one year of acquisition). With it, you can tailor revenue to fit your demands and create revenue that lasts forever. Deferred annuities: For those who intend to expand their money over time, but are willing to postpone accessibility to the cash till retirement years.

How much does an Retirement Income From Annuities pay annually?

Variable annuities: Supplies higher capacity for growth by investing your cash in financial investment choices you pick and the ability to rebalance your portfolio based upon your choices and in such a way that straightens with changing financial goals. With fixed annuities, the company spends the funds and supplies a rates of interest to the customer.

When a death claim occurs with an annuity, it is essential to have actually a called recipient in the agreement. Various choices exist for annuity survivor benefit, relying on the contract and insurance company. Picking a refund or "duration certain" alternative in your annuity offers a fatality advantage if you pass away early.

What is included in an Annuity Investment contract?

Calling a recipient various other than the estate can aid this procedure go extra smoothly, and can aid guarantee that the profits go to whoever the individual desired the cash to go to instead than going via probate. When present, a fatality benefit is automatically included with your agreement.

{kind=link}

Table of Contents

- – What are the top Variable Annuities providers ...

- – What is the difference between an Retirement I...

- – Is there a budget-friendly Guaranteed Income ...

- – Can I get an Guaranteed Return Annuities online?

- – How much does an Retirement Income From Annu...

- – What is included in an Annuity Investment co...

Latest Posts

Decoding Fixed Vs Variable Annuity Pros And Cons Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Benefits of Choosing the Right Financial Plan Why C

Breaking Down Your Investment Choices Key Insights on Your Financial Future What Is Fixed Annuity Vs Equity-linked Variable Annuity? Pros and Cons of Various Financial Options Why Annuities Variable V

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Fixed Annuity Vs Variable Annuity Defining the Right Financial Strategy Pros and Cons of Choosing Between Fixed Annuity

More

Latest Posts